How fees can eat into your returns

Vanguard founder John Bogle once said, "The more the manager takes, the less the investor makes." Though this appears to be quite obvious, what is much less obvious is the huge impact that fees can have on an investor's returns over the long term.

The impact of ETF management fees

To illustrate this point, let's start by looking at the fees within ETFs, in particular the Management Expense Ratio (MER).

With more than 350 ETFs listed on the ASX, MERs can range from as little as 0.03% up to a high of 1.89%, with the average MER around 0.55%.

Index-tracking ETFs typically have the lowest fees, whilst active or strategy-based ETFs usually have higher fees.

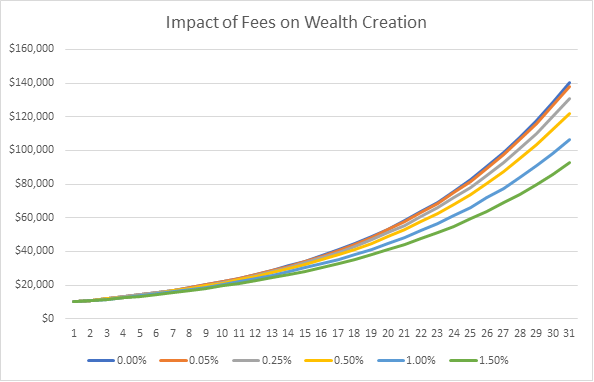

Fees can have a huge impact on long-term wealth creation and the following graph shows a range of different fee scenarios with MERs ranging from 0.05% to 1.50%. I have also included a "no fee" scenario which helps to show the total growth possible without fees.

For all scenarios, the initial investment is $10,000, and the fund grows (before fees) at 9.2% a year, the average total return of the All Ordinaries over the past 30 years.

As you can see, there are sharply different outcomes for each MER. What is most surprising though, is that with high fees, the lost opportunity is immense.

The table below shows the outcomes for each scenario at the end of the 30 years. I have also included the percentage of the total growth opportunity that's lost to fees. The total growth opportunity is seen in the 'no fees' scenario and is $130,178.

|

MER |

Balance after 30 years |

Lost opportunity due to fees |

% of total growth opportunity lost to fees |

|

0.00% |

$140,178 |

$0 |

0.0% |

|

0.05% |

$138,265 |

$1,913 |

1.5% |

|

0.25% |

$130,863 |

$9,315 |

7.2% |

|

0.50% |

$122,148 |

$18,030 |

13.9% |

|

1.00% |

$106,370 |

$33,808 |

26.0% |

|

1.50% |

$92,570 |

$47,608 |

36.6% |

Assumes a starting balance of $10,000 and return of 9.2%p.a.

The above table shows that for an MER of 0.05%, the percentage of the total growth opportunity lost to fees over 30 years, is a moderate 1.5%.

However, for an MER of 1.50%, the total growth opportunity lost to fees over 30 years, is a staggering 36.6%. The difference between the two equates to $45,695.

The reason for this surprising result, is that when money leaves your compounding process every year via fees, that specific money can no longer compound.

Compound interest

Compound interest refers to how a sum of money grows, as interest is applied to both the principal amount and the accumulated interest.

A quote often attributed to Albert Einstein is, "Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it."

However, an even better quote comes from Bogle, who said, "Keep your investment expenses low, for the tyranny of compounding costs can devastate the miracle of compounding returns."

These compounding costs that Bogle refers to, are fees. Once fees leave the compounding machine, they can no longer compound. Hence, money paid out in fees in Year 1 and 2 etc, are lost multi-decade opportunities for compounding.

Capital gains tax

In addition to management fees, there are other ways for money to leave your compounding process, such as through capital gains tax and brokerage fees.

The capital gains tax on an investment can be quite significant, especially if that investment has performed well for a long time. That's why selling out of one investment and buying into another, isn't always the best financial move.

For example, if you are considering selling an ETF with a MER of 0.05%, to buy another ETF with a lower MER of 0.04%, it simply may not be worth it, due to the capital gains tax involved. Once you pay this tax, that money leaves your compounding process forever.

Brokerage fees

Brokerage fees are another expense that can eat into your returns. They can be a flat fee, a percentage based on the total transaction value, or a combination of both. Brokerage fees can range from $0 to $30 for online brokers or can start from around $70 for full-service brokers.

Let's say that an investor performs two trades per month for 30 years, at a cost of $15 per trade. Let's also say the average total returns of the market are 9.2%.

Over 30 years, if the investor had saved those brokerage fees, and invested in the market instead, they would be an incredible $50,939 better off. Now, of course, you need to trade to buy into the market, but the trick is to not overtrade.

A further consideration is the size of your brokerage fees versus the size of your investment purchase. If you pay high brokerage fees for a small investment, it could mean that your investment needs to grow by a couple of percentage points just to cover your brokerage fees.

Key takeaways

The impact of high management fees, capital gains tax, and brokerage fees can be significant when viewed over the long-term.

However, just like death and taxes, fees are an inevitable part of life. But if we can minimise them at every point, whilst still receiving healthy returns, it can lead to the building of significant long-term wealth.

As Charlie Munger said, "Getting wealthy is like rolling a snowball. It helps to start on top of a long hill. Start early and try to roll that snowball for a very long time."

And always try to minimise your fees.

Ready to start investing? InvestSMART has a range of diversified portfolios that all come with a capped management fee. If you'd like help selecting the right style of portfolio for you check out our free statement of advice quiz. It will show you which InvestSMART ETF portfolio may best suit your goals and investment timeframe.

Frequently Asked Questions about this Article…

Management fees can significantly impact your investment returns over the long term. Even small fees can add up, reducing the amount of money that can compound over time. For example, a Management Expense Ratio (MER) of 1.50% can result in losing 36.6% of your total growth opportunity over 30 years.

The Management Expense Ratio (MER) in ETFs is a measure of the total fees charged by the fund manager, expressed as a percentage of the fund's average net assets. MERs for ETFs can range from as low as 0.03% to as high as 1.89%, with index-tracking ETFs typically having lower fees compared to active or strategy-based ETFs.

Keeping investment fees low is crucial because fees reduce the amount of money that can compound over time. High fees can eat into your returns, leading to a significant loss of potential growth. As John Bogle said, 'Keep your investment expenses low, for the tyranny of compounding costs can devastate the miracle of compounding returns.'

Brokerage fees can also eat into your investment returns. They can be a flat fee or a percentage of the transaction value. Over time, frequent trading and high brokerage fees can significantly reduce your returns. For instance, saving on brokerage fees and investing that money instead could make you $50,939 better off over 30 years.

Compound interest is the process where the interest earned on an investment is reinvested to earn additional interest. It's important for investors because it allows your investment to grow exponentially over time. However, fees can disrupt this process by reducing the amount of money available to compound.

Switching ETFs to save on management fees might not always be beneficial due to capital gains tax implications. Selling an ETF with a slightly higher MER to buy one with a lower MER could incur capital gains tax, which might outweigh the benefits of lower fees.

To minimize investment fees, consider choosing ETFs with lower MERs, avoid overtrading to reduce brokerage fees, and be mindful of capital gains tax when switching investments. By minimizing fees, you can maximize the amount of money that compounds over time, leading to greater long-term wealth.

You can start investing with low fees by exploring diversified portfolios with capped management fees, such as those offered by InvestSMART. They provide a free statement of advice quiz to help you select the right ETF portfolio that aligns with your goals and investment timeframe.